VERRA MOBILITY (VRRM)·Q4 2025 Earnings Summary

Verra Mobility Q4 2025: Revenue Beats on NYCDOT Expansion, EPS Misses on Implementation Costs

February 24, 2026 · by Fintool AI Agent

Verra Mobility reported Q4 2025 results that delivered on the top line but disappointed on profitability. Revenue of $257.9 million beat consensus by 6.9%, driven by the NYCDOT red-light camera expansion and strong Commercial Services growth . However, Adjusted EPS of $0.30 missed expectations by 4.1% as implementation costs and NYCDOT readiness expenses compressed margins .

The quarter's highlight was securing a new $998 million, 5-year contract with NYCDOT, effective January 1, 2026, replacing the expired agreement . The company also returned $133.4 million to shareholders through share repurchases in Q4 .

Did Verra Mobility Beat Earnings?

Mixed results: Revenue beat, EPS missed.

The revenue beat was driven by strong execution in Government Solutions, where the NYCDOT red-light expansion contributed approximately $23.9 million in installation services revenue and $14.5 million in product revenue during Q4 . Total Government Solutions revenue surged 25% YoY to $129.2 million .

The EPS miss stemmed from margin pressure in Government Solutions, where segment profit margins contracted to 24% from 34% in the prior year quarter due to increased costs supporting project implementations and NYCDOT readiness activities .

How Did Each Segment Perform?

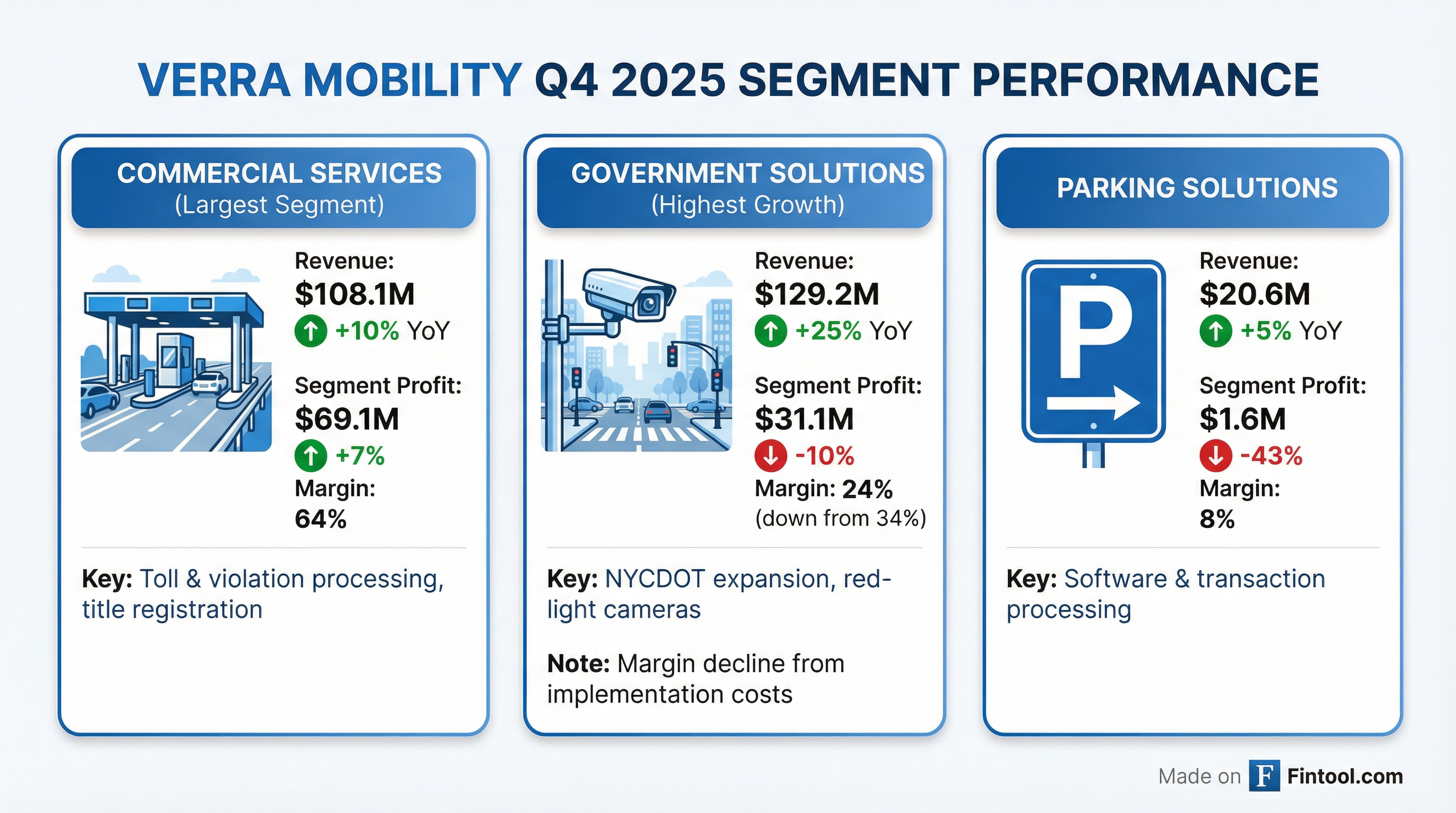

Commercial Services — Steady Growth

- Revenue: $108.1M (+10% YoY)

- Segment Profit: $69.1M (+7% YoY)

- Margin: 64% (down from 65%)

Growth driven by product adoption, tolling activity, and European operations, partially offset by prior customer churn in fleet management .

Government Solutions — High Growth, Compressed Margins

- Revenue: $129.2M (+25% YoY)

- Segment Profit: $31.1M (-10% YoY)

- Margin: 24% (down from 34%)

The margin contraction was expected as the company invested heavily in the NYCDOT camera expansion. Installation services revenue increased $13.7 million YoY, and product revenue jumped $5.9 million from the red-light program .

Parking Solutions — Modest Growth

- Revenue: $20.6M (+5% YoY)

- Segment Profit: $1.6M (-43% YoY)

- Margin: 8% (down from 14%)

Increased one-time product sales offset by lower SaaS and subscription services revenue .

What Did Management Guide for 2026?

Verra Mobility established the following guidance for fiscal year 2026 :

Key assumptions underlying the guidance :

- Diluted share count: ~155 million (down from 161M)

- Effective tax rate: 28-29%

- CapEx: ~$125 million (for camera installations and MOSAIC implementation)

- D&A: ~$125 million

- Interest expense: ~$62 million

The guidance implies EBITDA margin contraction from 42% to approximately 39-40%, reflecting the ongoing transition to the new NYCDOT contract structure, which has "materially different" terms including service level agreements, service credits, liquidated damages, and cybersecurity requirements .

Stock Price & Earnings History

VRRM stock has declined ~29% from its 52-week high of $26.38 to the current level of $18.71. The company has beaten EPS estimates in 7 of the last 9 quarters, with Q4 2023 and Q4 2025 being the misses.

What Changed From Last Quarter?

Notable changes:

- NYCDOT contract renewal secured — The old contract expired December 31, 2025, replaced by a new 5-year, $998M agreement

- Accelerated buybacks — $133.4M repurchased in Q4 alone vs. full-year total through Q3

- Debt refinancing completed — Extended term loan maturity to October 2032

- Net leverage improved — 2.3x vs 2.4x at year-end 2024

Key Management Quotes

CEO David Roberts on the quarter and outlook:

"We closed 2025 with strong execution and momentum across our three business segments... Looking ahead to 2026 and beyond, we are executing against a focused value-creation strategy designed to strengthen our core, enhance profitability and position Verra Mobility for durable long-term growth."

Capital Allocation & Balance Sheet

The company has $116.6 million remaining under its $250 million share repurchase authorization through November 2026 .

Full Year 2025 Summary

Note: FY 2024 net income was depressed by a $97.1 million goodwill impairment charge in the Parking Solutions segment .

Forward Catalysts

- NYCDOT margin normalization — Implementation costs expected to subside through 2026 as the camera installation phase completes

- Expanded buyback runway — With $116M remaining authorization and strong FCF guidance ($150-160M), continued capital returns likely

- European expansion — Management cited European operations as a growth contributor in Commercial Services

- MOSAIC implementation — Technology platform investment expected to drive operating leverage

Risks & Concerns

- NYCDOT concentration risk — The contract represents a material portion of revenue; new terms include stricter SLAs, service credits, and liquidated damages

- Legislative/political risk — Photo enforcement programs face ongoing political and public acceptance challenges

- Margin compression — Adjusted EBITDA margin declined from 46% in FY 2024 to 42% in FY 2025, with 2026 guidance implying further compression

- Parking Solutions underperformance — Segment continues to struggle with sub-10% margins and recent goodwill impairment